As Chinese tech companies push abroad, India has been a land of opportunity. But rising tensions between the two countries are starting to raise questions about the future of Chinese tech in India.

Much like China did in the early 2010s, India’s residents are rapidly turning to online services, creating fertile ground for ambitious startups to thrive. The country is also home to a vast, underserved market of often-rural consumers.

Chinese companies have taken notice, with investment in Indian startups surging to $4.6 billion in 2019, a twelvefold increase from 2016.

Expanding Empires

Expanding Empires is TechNode’s monthly data-driven newsletter looking at where and how Chinese tech majors are investing in up-and-comers around the world. Available to TechNode Squared members.

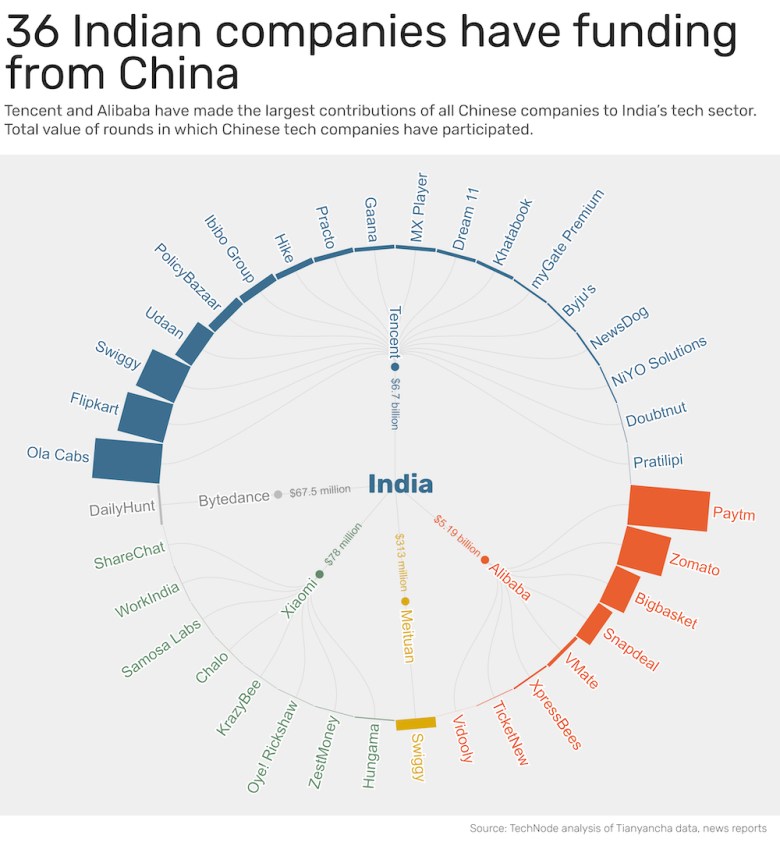

In the past five years, firms including short-video giant Bytedance, e-commerce firm Alibaba, social media behemoth Tencent, and smartphone maker Xiaomi have participated in funding rounds for Indian startups totaling more than $12.3 billion, according to my analysis of public data. These investments have helped to scale Indian unicorns like Paytm, Snapdeal, Swiggy, and Ola.

Now, however, these Chinese companies could be caught in the crossfire of a geopolitical battle. On June 29, Indian officials banned 59 Chinese apps over national security concerns—including apps made by companies that have been investing millions in the country’s startups.

India’s technology minister referred to the move as a “digital strike” against China. The ban came just two weeks after a deadly border clash between the two nations that left 20 Indian soldiers dead.

What is at stake for Chinese tech companies in India? This month, I’ve delved into the data to explore how intertwined India’s tech sector is with China’s. What has emerged is a story of a China tech proxy war, and investments that may come back to bite China’s biggest tech companies. Here’s what I found:

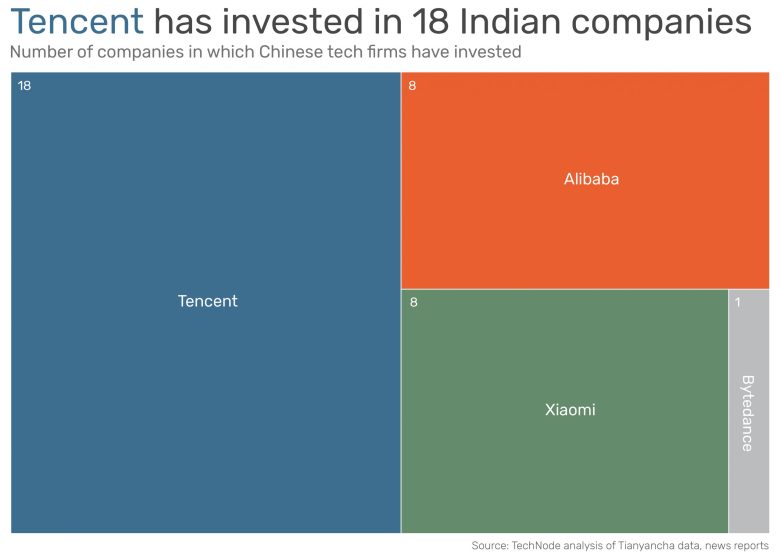

- Two companies—Alibaba and Tencent—dominate Chinese investment in India. Both are vying for a piece of India’s biggest tech companies.

- None of those companies have investment from both Chinese tech giants, dividing India’s tech sector into startups that are Tencent-invested and those that won investment from Alibaba.

- In the last five years, Chinese firms accounted for 11.6% of total funding to Indian startups, according to Mumbai-based think tank Gateway House, with 96% of this money being associated with Alibaba and Tencent.

- Several other companies, including Bytedance and Xiaomi, have also backed Indian startups, but to a lesser degree.

- The future of Chinese investment now looks uncertain as a result of rising political tensions between China and India.

Surging funds

China’s investment in Indian startups has swelled in the past four years.

The reason is due in part to rising suspicion of Chinese capital in the US, traditionally a popular destination for these companies. As American startups became a less-popular proposition, Chinese tech firms looked instead to Asia’s emerging markets.

Now, India’s popularity comes with a price tag.

Apps produced by Bytedance, Alibaba, Tencent, and Xiaomi were among those banned by India’s government at the end of June.

Bytedance’s massively popular short-video platform TikTok and its India-focused social media platform Helo have been blacklisted. Meanwhile, around eight of Tencent’s apps have been banned, including the popular messaging app WeChat, which has more than a billion users around the world, and seven QQ apps, including QQ Music and Wechat predecessor QQ messenger.

In addition, Alibaba’s popular UC Browser and UC News apps, as well as Xiaomi’s Mi Call app have been outlawed.

A tale of two companies

Five years ago, India looked like a safe place for a Chinese company to invest and earn profits. That’s when Alibaba made the first move into India.

In 2015, the company invested in the Indian startup payments Paytm through its fintech affiliate Ant Financial.

This wasn’t Alibaba’s first overseas investment. However, it did represent an important shift for the company, moving its focus away from investing in the US in favor of the developing markets of India and Southeast Asia—a strategy that now defines its approach to investing abroad.

Tencent followed suit later that year, becoming one of several investors to take part in a $90 million funding round for the medtech startup Practo.

Five years later, the two companies have become China’s biggest investors in India. Alibaba and Ant Financial have taken part in 20 funding rounds for Indian companies. The combined value of these deals exceeds $5 billion.

Meanwhile, Tencent has participated in rounds totaling a combined $6.7 billion in India. Of the nearly 180 international rounds in which Tencent has taken part, 24 were in India.

Chinese firms accounted for 11.6% of the total funding to Indian startups in the last five years, according to Gateway House. Tencent and Alibaba alone make up a significant portion of this total, according to my analysis. The value of the rounds that Tencent and Alibaba participated in make up 96% of the total value of all rounds in which Chinese tech giants have taken part in India.

Through these investments, the companies appear to be dividing up India’s fintech and e-commerce sectors. On one side are the Alibaba-affiliated companies: Bigbasket, Paytm, and Snapdeal. On the other side stand the Tencent-invested firms: Swiggy, Khatabook, and Flipcart.

Alibaba had initially focused its attention on smaller bets on companies in mature markets, but they changed tack in 2015. In India, the company has set its sights on well-established companies central to its core business, the majority of which were Series C or above at the time of investment. Its strategy has paid off. Five of its investments in India have reached unicorn status.

Tencent has pursued a different strategy. The social media giant has taken more of a shotgun approach, investing in a wide array of industries from content and entertainment to online travel to digital security.

Wider focus

Aside from Alibaba and Tencent, several other Chinese tech firms have pushed into the subcontinent by expanding their services to Indian users and investing in the country’s startups.

With perhaps the largest physical presence out of all the Chinese tech giants, Xiaomi has seen its India revenue surge. The company holds the largest share of India’s smartphone market: nearly 30% as of mid-2019.

In the third quarter of that year, the company reported that one-third of its revenue came from its India operations. The country is so important to Xiaomi that they even have an India-focused smartphone brand, Poco, which it spun off earlier this year.

Since the beginning of June, Xiaomi has even begun sporting a “Made in India” section on its Indian website, claiming that 99% of all the phones it sells in the country are made there. The move is part of a 2014 plan by the Indian government to incentivize manufacturing within the country.

Aside from its own products, Xiaomi has also invested in several Indian startups, participating in eight funding rounds worth a total of $78 million.

These investments have predominantly focused on early-stage companies offering mobility and content and entertainment services. Investments in digital services make sense in a country with a rapidly growing internet population. Xiaomi describes itself as an internet company despite the fact that the majority of its revenue is derived from hardware.

Xiaomi has predominantly focused on India, with just one US-based startup in its portfolio, while a third of all international funding rounds in which Bytedance has participated involve Indian companies.

Bytedance’s investments come as the company has pushed its own services—most notably TikTok—in India. The content giant has invested $67.5 million in Dailyhunt, an Indian news aggregator.

But it’s Bytedance’s own apps that make it a big deal in India. The country is TikTok’s biggest market, boasting around 200 million monthly users. Bytedance also operates the Indian social media platform Helo, which had nearly 50 million monthly users last July, according to the company.

Souring relations

Rising tensions between China and India are threatening to bury Chinese companies’ early success on the subcontinent—and any future investments—in an unexpected geopolitical earthquake. India is taking steps to limit Chinese foreign direct investment in the country over concerns that the companies are state-owned.

Apart from blocking Chinese companies’ apps, India amended its foreign direct investment (FDI) rules earlier this year. The amended rules require any company from a bordering nation to get permission from the government before investing in an Indian company. The rules had previously only applied to Pakistan and Bangladesh.

Changes to India’s FDI laws are likely to have a “detrimental effect” on India’s startup ecosystem, according to Aurojyoti Bose, lead analyst at Globaldata. “Chinese companies have traditionally been the lead investors in some of the key startups in India, which also enabled these startups to scale up,” said Bose.

The new rules, coupled with tensions on the border and rising nationalism within the country, appear to have motivated the government’s move to ban the 59 apps.

The app ban, as well as the changes to investment laws, are raising questions about the future of Chinese tech in India. US companies already appear to be taking advantage of this. This week, Google announced that it would invest $10 billion in India, including equity investments, over the next five to seven years.

With no ceasefire in sight, Chinese companies with their eyes on India may start looking elsewhere for their next big investment.